Interview: Nirmal Jain: 'There are concerns, but not too many alternatives to India too'

Interview: Nirmal Jain: 'There are concerns, but not too many alternatives to India too'

So let us look at two facts. One, India is the fastest growing economy and the best market to invest in as well as in terms of growth in the world today. But regardless of that, whatever the best market, there is some value and beyond that investors start getting worried. It is human psychology to compare. Indonesia is doing very well, and Vietnam is doing very well but they are smaller markets.

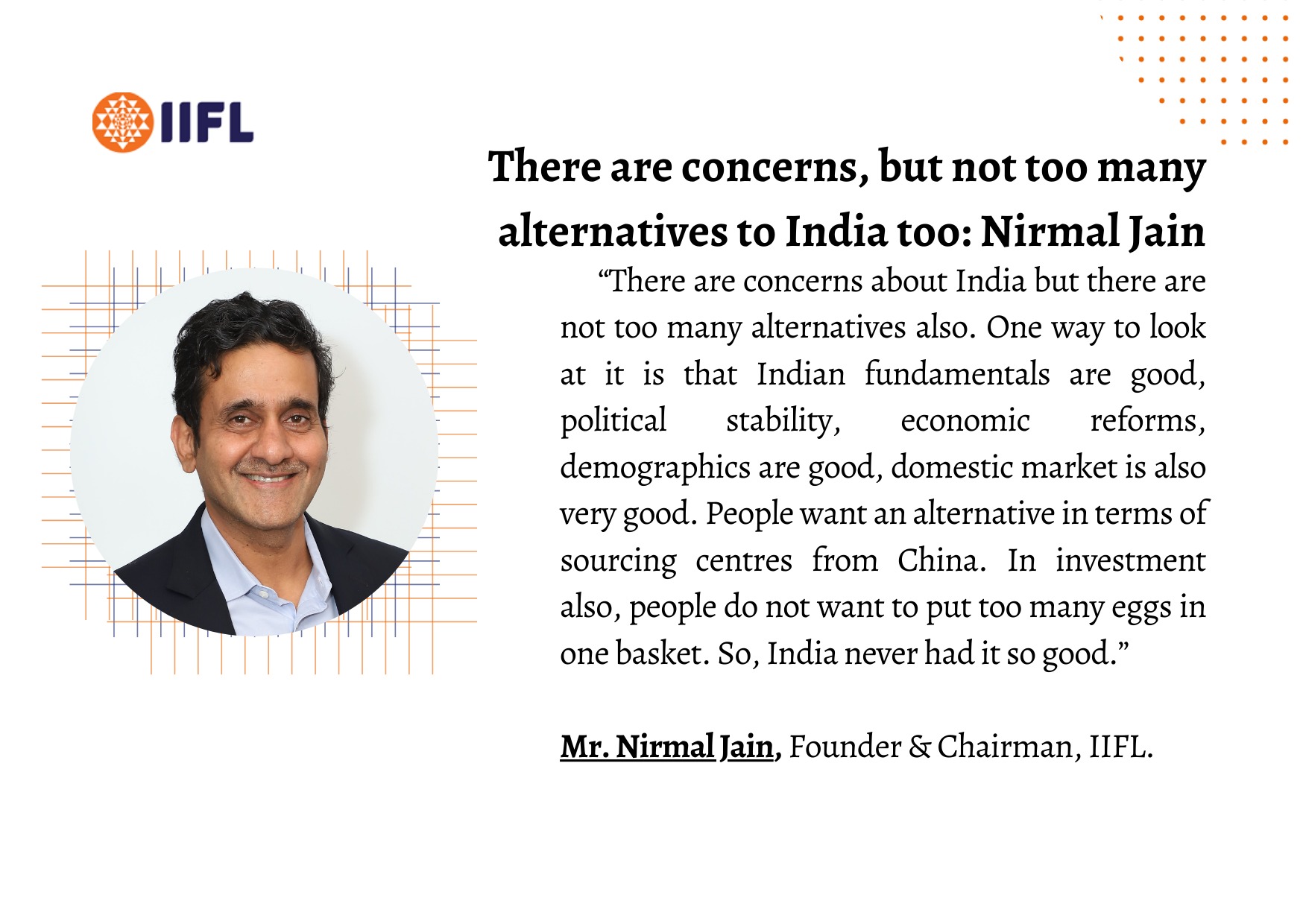

So there are concerns about India, but there are not too many alternatives. One way to look at it is that Indian fundamentals are good, politically stable, economically reformed, and demographics are good, the domestic market is very good and people are getting disillusioned by China’s growth which has been a little opaque. People want an alternative in terms of sourcing centres from China. In investment also, people do not want to put too many eggs in one basket. So, India never had it so good.

On RBI announcement banning third-party loan recovery by NBFCs

The collection mechanism primarily should be done in-house as that way, there can be a code of conduct. A company can have certain policies and what your people can and can not do so that there is a rule of law in this country by which everybody should abide.

Whether somebody is a defaulter or not, one can have legal remedies available, and I firmly believe that all lenders have to follow the law. Nobody is above the law. Even if the gravest of crimes happened, you cannot impart justice. Justice can only be imparted by the court, but sometimes there can be some stray and exceptional cases, I do not know about this particular case. But the fact of the matter is that if there are collection agents, and they are incentivised based on the collection amount, then they tend to be aggressive.

So collection agents should be used very sparingly and primarily for larger wilful cases if at all, even they should be very carefully empanelled based on their legal processes. Many Chinese apps were using socially coercive methods. Some people came and told us that we give loans and we get the entire contact book so we can target the people that they talk most to, which will be family members or whatever.

We never accepted those kinds of things because you cannot intrude into anybody’s privacy in that manner. There is a code of conduct which every company will have to follow, and that way, there will be lesser problems, it will go a long way, and you will also grow faster.

What is your take on technology as an enabler to not only disburse loan but collect it more efficiently also so not only are your costs lower but the collection flow is also monitorable?

Tech is a huge solution. What we do is that we focus on small ticket loans. In small ticket loans, it runs like a process, and that process should be good so that your NPAs are less, the legal notices are also automated, and you do not have to do much because for a small loan, it is not worth your while to go after the customer.

So it runs by process and numbers. You know that a certain percentage will go bad and that you will provide for but technology is very useful for monitoring the defaults happening anywhere else. Sometimes the DSAs (direct sales agents) can do fraud. Suppose you are a customer, you have not taken any loan and with your salary, you are eligible for say Rs 1 lakh loan. Some DSAs will promise to give Rs 5 lakh loans. You will say that because the income does not justify that, but you are greedy, and you may accept it. So they can get you five applications simultaneously. Now what will happen is after a month or two, all five of them will discover what happened to this customer, he is overburdened. But there are systems and processes to do, to take care of everything and the good thing about India is that the account aggregator, the digital technology is giving data access digitally at such low cost and if you use it effectively, it can be wonderful for everything, even for collection and serving the customer.

Also, now the Sarfaesi law allows you to purchase a property much more easily than in many other countries. In India, the legal infrastructure is coming, we should not have the mindset of the past that the legal framework is weak, and we should use that.

How are the various segments of your current business – SME, gold loan, home loan doing? Traditionally retail loan demand surges between now and Holi. What are the initial inquiries data telling you about the demand front?

Demand is doing very well and has bounced back. What is happening is that credit collection, as well as demand, are improving from MSMEs. Even home loan demand has improved very well, but when the interest rate increases, home loans are affected as EMI is dependent on interest rates. If EMIs go up, people may defer home purchases. Right now, the income levels are going up, people are seeing salary increases, business is doing very well and so we are not seeing any impact on demand but we are watchful.

Are you confident of your earlier growth targets of 25%, one lakh crore in the next couple of years in your loan book? Are you confident of that or will you review it in the next few years because of the global slowdown impact on India?

At this point, we are very confident and optimistic that things are going the right way. But if something unforeseen happens, we have to review the way things stand today, the underpenetrated credit market, and the way we partner with banks and complement them is crucial. India is a huge economy; it is a $3 trillion economy. So when we are talking about say Rs. 1 lakh crore, it is maybe $12-13 billion which is not even a fraction of what the market is. So we are fairly confident.