Trust Checkr

Fraud Pre-Emption

Platform

The Challenge

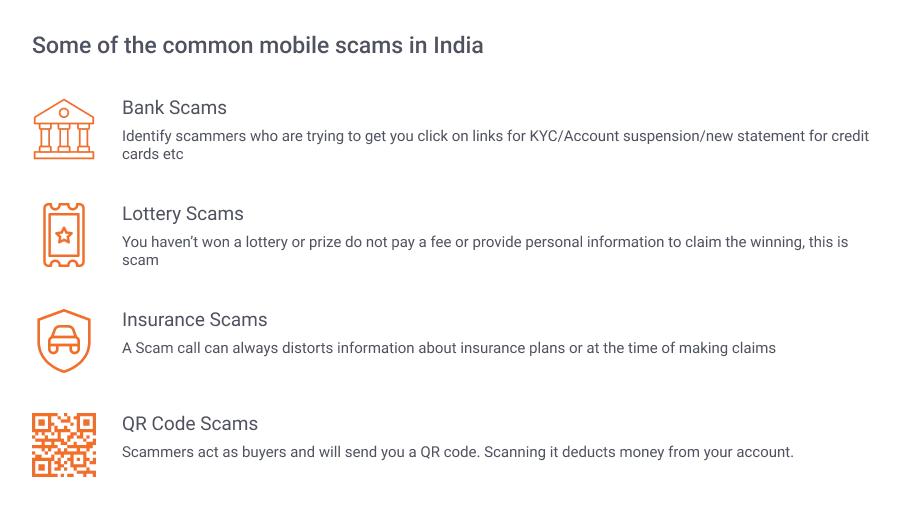

As per the Federal Trade Commission, identity theft complaints accounted for ~24% of the total fraud, identity theft, and other complaints received. Identity theft can happen in many ways: Phishing, smishing, spoofing, and vishing are some techniques Fraudsters use.

In the year 2021,

1. More than 5.8 million fraud complaints were filed for the FY22, an increase of 19% YoY.

2. The financial losses from fraud increased by 77% from the previous year to more than $6.1 billion.

3. Consumer identity theft complaints increased by 3.3% to just over 1.43 million.

The process of detecting stolen identities begins at the onboarding stage. Adding new customers can be risky for banks regarding digital onboarding – there is the need to satisfy regulations such as KYC (know your customer) and AML (anti-money laundering). These legal obligations must be obeyed to prevent any kind of financial fraud. Criminals often use false or synthetic IDs to deceive the process and open bank accounts, so confirming identities can be expensive – with costs reaching $35.2 billion in 2020. This is especially daunting for neobanks and challenger banks, who strive to make the customer onboarding experience quick and straightforward.

Market

As the digital payments landscape in India continues to expand, its growth is not only evident in the sheer number of transactions and the substantial amount of money being processed, but also in the increasing presence of banks and NBFCs within this ecosystem.

According to a report from Statista, India's digital lending market surged from $9 billion in 2012 to $150 billion in 2020, and it is projected to reach $350 billion by 2023.

Hence, security emerges as a pertinent apprehension within the expanding ecosystem, given that fraudulent activities linked to digital payments are gaining speed and sophistication in tandem with technological progress. Among these fraudulent practices, credit-related scams are particularly prevalent. These involve the creation of counterfeit profiles by malicious actors who obtain credit and subsequently vanish, causing significant distress to both financial institutions and NBFCs.

It is expected that the market for identity and access management (IAM) products in India will increase from USD 83 million in 2019 to USD 130 million in 2022, at a CAGR of 16.3%.

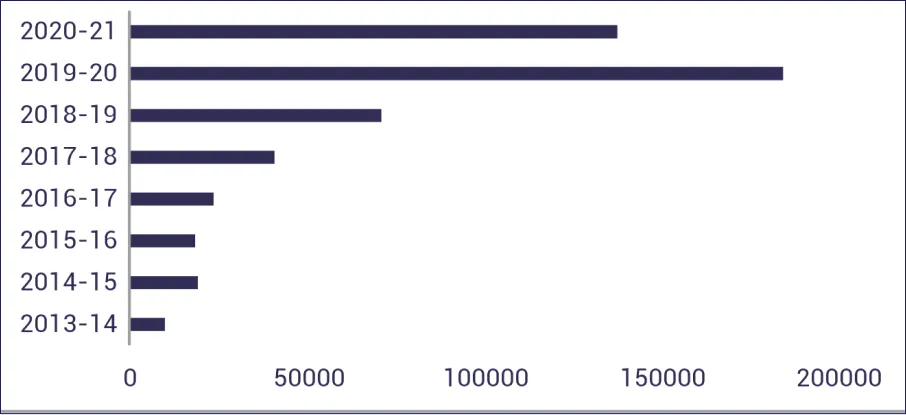

BANK FRAUDS IN INDIA (INR Cr)

The Solution

Trustcheckr enables businesses to identify fraud, fake or bot profiles using image processing and artificial intelligence at the entry level itself.

The platform assists companies recognise toxic emails and know more about their customers with the help of more than 15 public application programming interfaces (APIs), including Facebook, Twitter and Foursquare, besides other date-paid and public sources.

The solution could serve businesses across industries, including fintech (social scoring for first-time loan seekers), dating (identifying fake or fraud profiles) and e-commerce (increasing marketing campaign efficacy). TrustCheckr was part of global startup incubator NUMA Season 3 acceleration programme.